23 Jan 2019 A difficult year for many Alternative UCITS funds

Many Alternative UCITS funds did not have a happy 2018. Only one in six funds was able to post positive results for the year and assets under management in the total space declined with slightly less than 8%.

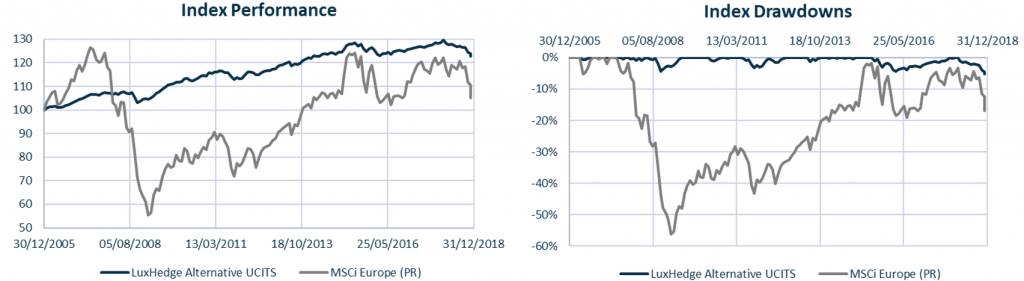

The LuxHedge Global Alternative UCITS Index posted a loss of -4.45% in 2018, the worst annual result since the start of the LuxHedge indices in 2006. Every strategy group index lost and dispersion between funds was even larger than usual with the top performers delivering uncorrelated double digit returns to investors, being rewarded by some of the largest inflows that we’ve witnesses the past years.

The graphs below aim to put things in a broader historical context, showing annual returns for the LuxHedge Alternative UCITS index (EUR) versus the MSCi Europe Index (EUR) since 2006. 2018 was an exceptionally bad year with a larger beta than usual and the equal weighted fund index not delivering any alpha at all. In a simple regression since 2006, the index has a beta of 14% and annual alpha of 1.3% with respect to the MSCi Europe.

Within Equity Hedge strategies, both Long/Short Equity (-6.3%) and Equity Market Neutral funds (-3.97%) lost a lot of ground. Fixed Income Alternative strategies are in negative terrain as well but have shown most resilience and decorrelation in 2018 with the Rates Long/Short Index ending the year at -1.02% and Credit Long/Short Index at -2.66%.

The largest annual losses were realized by quantitative multi asset strategies with the LuxHedge CTA Index declining -6.46% and the LuxHedge Alternative Risk Premia Index declining -6.74%. Looking at the average fund, Alternative Risk Premia turned out to be the worst performing strategy in 2018, exactly at a time when many investors increased their allocations. Out of the 36 constituent funds in the Alternative Risk Premia UCITS Index, only one was able to end the year with a positive result.

Within the universe of 135 Alternative Fund of Funds, no fund was able to present a positive performance in 2018. The average fund as measured by the LuxHedge Alternative Fund of Fund Index declined -5.33%.

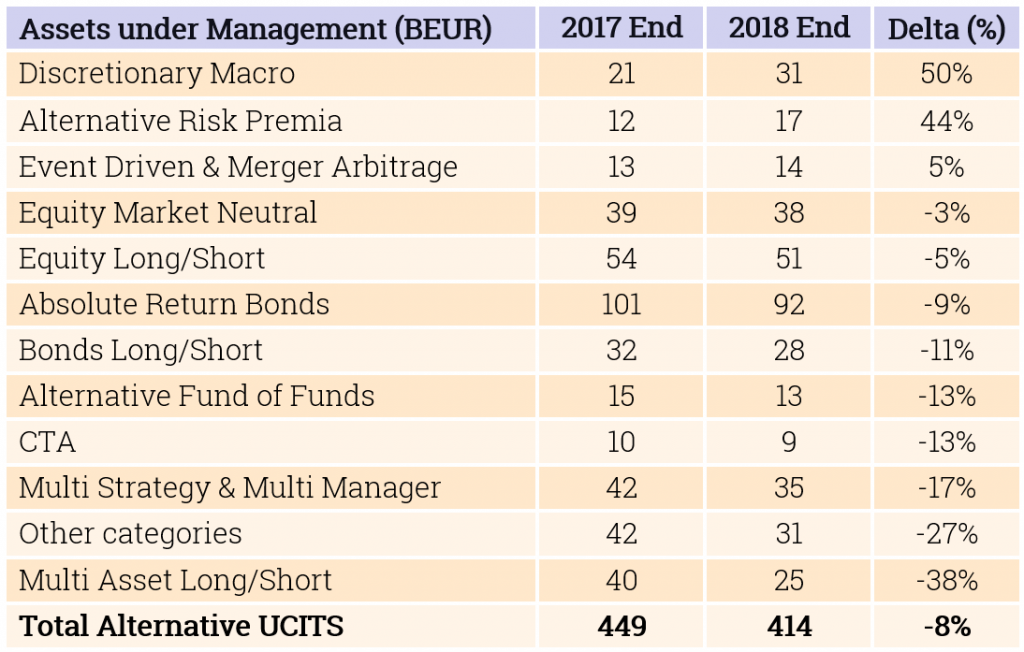

Assets under Management in the overall universe declined with -7.9% during 2018. Most of the decline is explained by negative performance, but 2018 was also the first year since 2008 where Alternative UCITS funds experienced outflows.

Diversified funds allocating to different managers and strategies lost -13% (Fund of Funds) and -17% (Multi Strat & Multi Manager) of assets, perhaps suggesting that many allocators preferred selecting strategies themselves at a time when this mattered most.

Multi Asset Long/Short funds saw the biggest decline in capital and lost 15MEUR in AUM last year (-38%). This mainly represents one of the largest and oldest Alternative UICTS funds that disappointed during 2018, losing a lot of its long standing appeal.

Discretionary Macro funds on the other hand had a very successful 2018 in terms of asset growth with a 10BEUR AUM increase, largely driven by a well-known French/UK macro boutique that continued to outperform peers. Also Alternative Risk Premia funds continued to attract inflows throughout the year, despite disappointing performance overall.

Event Driven and Merger Arbitrage strategies grew in assets as well with the bulk of inflows going to a very select group of outperforming Merger Arb specialist funds.

For further details, please refer to monthly LuxHedge Market overviews