18 Sep 2018 Alternative UCITS funds slide further in August, US Equity Hedge strategies outperform

Close to 60% of Alternative UCITS funds posted losses in August, pushing broad based indices lower. The LuxHedge Global Alternative UCITS Index lost -0.41%, bringing 2018 YTD to -1.43%. Only one quarter of all funds is currently able to post year-to-date positive figures.

Equity Hedge strategies focussing on the US stock market are a notable exception with the LuxHedge Equity Long/Short US Index advancing +1.13% in August (+2.44% YTD). This is not only due to a long market bias, also Equity Market Neutral US funds are able to create alpha and are up +2.30% since beginning of the year. With quantitative easing well beyond us and correlations between single stocks declining more and more, active long/short US stock pickers are doing well.

Most other Equity Hedge strategies lost during the month of August: LuxHedge Long/Short UCITS Index -0.43% (-0.51%). After a great 2017, Emerging Market Long/Short managers are going through much tougher 2018 conditions with the LuxHedge Long/Short AP & Emerging Market Index losing -1.97% in August, losses already adding up to -5.20% YTD. Equity Market Neutral funds remained relatively flat in August (+0.11%).

All Fixed Income Alternative strategies lost some ground too: Credit Long/Short -0.21%, Rates Long/Short -0.81% and Absolute Return Bonds -0.62%. Discretionary Macro strategies had one of the worst months in a long time (-2.72%) while systematic CTA UCITS showed solid gains of +1.26% in August.

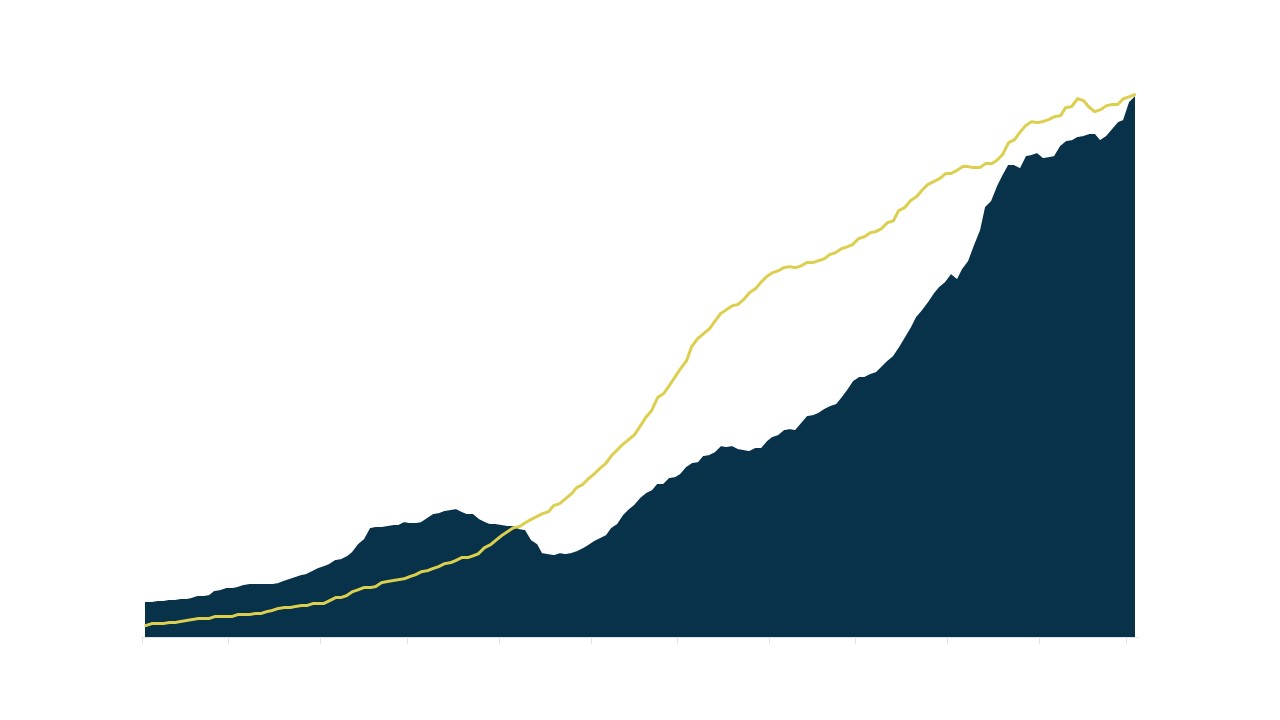

Asset Flows

Against the backdrop of trade tensions, Emerging Market turmoil, Brexit uncertainties and political struggles in Europe, risk aversion is clearly rising in 2018. Since beginning of the year, investors have allocated an extra 5% to Alternative UCITS funds in order to de-risk and diversify their portfolios. The asset inflow has not been evenly distributed across strategies through and it is particularly insightful to have a deeper look at which categories are currently popular.

Under the current market circumstances, Multi-asset Alternative strategies attract most capital. Discretionary Macro managers (Global Macro + EM Macro) were able to increase their assets by a whopping +40% since beginning of the year. Also Multi Asset Absolute Return funds gained +20%. Within systematic multi-asset strategies, Alternative Risk Premia UCITS continue their steep upward path and attracted 36% of fresh capital in the past 8 months.

Within Equity Hedge strategies, investors clearly prefer being completely hedged via market neutral solutions. Where Equity Long/Short strategies increased their AUM with +5% (in line with the global Alternative UCITS market), Equity Market Neutral funds have seen their assets under management rise by +10%.