08 Oct 2018 Manuel Kalbreier Investment Director Wellington

Manuel Kalbreier is an Investment Director at Wellington and Heads the Alternative Investments activities for EMEA. In February of this year, Wellington partnered with Schroders to launch their multi-strategy Hedge Fund Pagosa in a UCITS form. LuxHedge had an interview with Manuel to talk about Wellington Management and the different alternative strategies used in the Pagosa fund.

LH: Can you please introduce Wellington to us?

Wellington: Wellington Management was founded in 1928 and currently manages approx. USD 1 trillion of assets*. We have only one business, which is active asset management for our clients. We believe that the key to our success is generating long-term alpha for our clients, which we can realise if we have talented portfolio managers, global industry analysts, macro analysts and quantitative research. We are very focused on attracting and retaining talent to create an environment that adds value for our clients.

*Wellington Management as at 30 June 2018

LH: How are you set up to attract and retain talented professionals?

Wellington: Human capital is everything in this industry. Our firm’s partnership structure is designed to foster a culture that is collegial and stimulating, where independent thinking is valued and ideas can be freely shared and respectfully debated. We believe this improves the quality of investment decisions, as well as making Wellington an enjoyable place to work. That, and the incentives of the partnership structure, means that our most talented people tend to stay at Wellington for many years, using their experience to deliver effective investment solutions for clients. For example, our very first alternatives strategy is still running under the same manager, 24 years after it was launched.

LH: How big is the alternatives business at Wellington?

Wellington: Alternatives are a key part of our business. The alternatives team started in 1994 and currently manages approx. USD 40 billion * across 75 alternative strategies.

*Wellington Management as at 30 June 2018

LH: Looking at Schroder GAIA Wellington Pagosa, what are your high-level targets? What do you want to achieve in terms of returns, volatility and correlation?

Wellington: Schroder GAIA Wellington Pagosa is a multi-strategy fund that seeks to generate consistent positive returns across a market cycle, carefully managing different risk exposures. We aim to deliver to clients a consistent return stream that is relatively uncorrelated to market betas and, importantly, seeks to provide downside mitigation when market activity is more volatile. We are looking for 6% to 8% annualised net returns with about 5% to 7% volatility over a market cycle.

Crucially, we aim to reduce our market exposure and reliance on beta to generate returns. While we don’t want any of the strategies in the Fund to rely on a structural market beta, some strategies, like equity long/short or credit long/short, have some beta exposure on average, but these exposures will be entirely tactical.

LH: By tactical, do you mean that the portfolio managers of the different underlying strategies might take their beta down to zero if they feel that it is appropriate

Wellington: Yes, exactly. The aim is for all of the underlying portfolio managers to either be market neutral or have temporarily low beta for tactical purposes. The historical equity beta of the Fund is 0.3, and the interest-rate duration is well below a year.

LH: Can you give a high-level flavour of the different sub-strategies that constitute Schroder GAIA Wellington Pagosa?

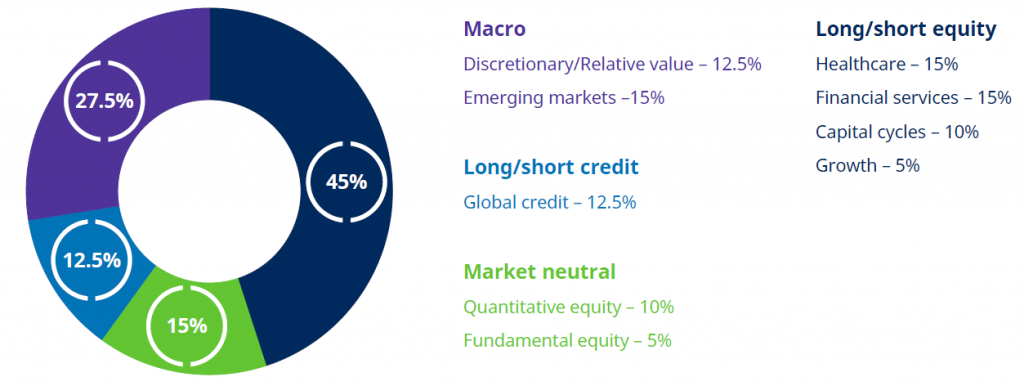

Wellington: The best way to visualise the nine underlying strategies is to think about the four big buckets to which we allocate capital for Schroder GAIA Wellington Pagosa (as at 30 June 2018).

• Macro (currently representing 27.5% of the total portfolio) is divided between emerging markets macro and developed markets macro strategies

• Long/short credit (12.5%)

• Equity market-neutral (15%), where we currently have two strategies

• Long/short equity strategies (45%), where we currently have four strategies.

I think about our portfolio as being split between two big areas, equity and fixed income. Within this, we have a mix of different strategies that are either completely market neutral or can be more tactical in their beta allocation.

LH: Before we move into detail on the underlying strategies, can you give us your view on the competitive edge that Wellington has in managing a multi-strategy fund? Is there anything that makes the Fund unique in your opinion?

Wellington: The key to making a multi-strategy proposition successful is the ability to pick strong underlying strategies and weave them together in a coherent portfolio. At Wellington, we have 75 different alternative strategies managed in-house. We can perform deep analysis with real track records and all the information necessary to decide whether to include a manager in the multi-strategy proposition. I think it’s relatively unique to be able to pick from so many alternative strategies with such a long track record.

Wellington is also taking the netting risk for the performance fee on a total fund level (LuxHedge note: an investor will only be charged a performance fee on the total portfolio level. Some multi-strategy funds would charge a performance fee for each of the different underlying strategies, sometimes resulting in a performance fee to be paid on some underlying strategies while the total portfolio performance is negative.).

LH: Can we dive a bit deeper into the two macro strategies and how they fit into the total Fund portfolio?

Wellington: Within macro, we allocate to an emerging markets (EM) and a developed markets (DM) strategy. The EM macro strategy launched at Wellington for institutional investors in 2006. It is currently closed to new investments and is only available to clients through multi-strategy solutions, like Schroder GAIA Wellington Pagosa. Next, we have a developed markets macro strategy that is a mix of relative-value G7 rates, foreign-exchange (FX) and quantitative approaches.

The macro bucket fits nicely into a multi-strategy allocation. In my opinion, macro has been a relatively difficult place to make money in recent years, because of the unusually low interest-rate environment. We are currently seeing increases in interest rates, volatility and policy divergence across central banks. This is driving a pickup in the performance of our G7 macro approaches, which historically have tended to perform quite well when other equity-oriented strategies have performed poorly. In this respect, I believe macro is a good building block in our multi-strategy portfolio.

LH: Looking at the long/short credit allocation, how is this strategy managed and how do you see it being positioned towards the future?

Wellington: This is a really interesting building block for a multi-strategy fund, because we’re in an environment with tight credit spreads, while interest rates are picking up again. In broad terms, the team expects that, as interest rates rise and it becomes more expensive for companies to service their debt or issue new debt, default rates and credit spreads are likely to move up again as well. We think this is going to lead to quite a bit of diversification between those credits that will be fine and others that will experience difficulties, within both investment grade and high yield. Looking ahead, we think we will probably be in a supportive environment for long/short credit strategies.

LH: Is this a portfolio of long credits with a short exposure to bond indices, or do you also short single-name credits?

Wellington: Within long/short credit, we have three different sub-strategies, two of which use short exposures to single-name credits.

The first sub-strategy is a pure relative-value play that looks for pairs of credits which used to trade quite close to each other but are now dispersed. When we think that there’s a reason for the two credits to likely converge again, we set up a relative-value long/short trade. Consequently, this sub-strategy will typically have a very low credit-spread duration.

The second sub-strategy takes a directional view on credit, picking companies on a standalone basis on both the long and short side, based on our views on whether the particular credit is likely to widen or tighten. With trades on the long and the short side, this part also has a relatively low overall credit-spread duration.

The last sub-strategy within long/short credit is much more tactical, taking a macro view of where we stand in the credit cycle. This part will have a tactical beta to credit.

LH: Can you please talk us through the equity market-neutral strategies used in the Fund?

Wellington: The 15%* market-neutral allocation is a really powerful addition for a multi-strategy fund because it has zero beta by construction. We allocate to two very different market-neutral approaches, one quant and one fundamental.

The quant strategy has a six-year track record and thinks dynamically about the underlying stocks that compose the different factors, such as value and growth. For this reason, it is also highly capacity constrained. At the other end of the market-neutral spectrum, we have a fundamental strategy with a thematic approach. Based on our company research, this strategy picks the most differentiated themes to construct a portfolio that is completely market-, sector- and factor-neutral. The quant and fundamental approaches are very different, potentially providing good diversification.

* Schroder GAIA Wellington Pagosa as at 30 June 2018.

LH: The last big bucket that you allocate to is long/short equity. Can you please give an insight into how you choose the strategies for the Fund?

Wellington: We currently have a 45% total allocation across four different long/short equity strategies. Within this, we select managers who take some tactical beta exposure. We are looking first for established managers with a track record going back at least five years. The second criterion is a demonstrated ability to be tactical in the beta allocation. For example, we might look for a thematic healthcare strategy which had a positive performance at times when the healthcare sector was down substantially.

LH: Next to healthcare and financials thematic long/short, there is also a capital cycles strategy. What is the underlying philosophy there?

Wellington: Our capital cycles strategy portfolio manager used to be a natural resources global industry analyst at Wellington before launching the approach about five years ago. The investment philosophy stems from a well-known phenomenon in natural resources, where prices tend to mean revert. At the top of the cycle, when prices are high, there tend to be new industry entrants and abundant company capital expenditure (capex) investments. These naturally lead to some overproduction and lower prices over time. At the bottom of the market, companies leave the sector, go bust or cut capex as much as possible. The reduced production will mechanically lead to higher prices. The capital cycles strategy uses this framework across lots of different sectors in many global markets, not just natural resources.

LH: Finally, can you outline the growth equity long/short strategy within the Fund?

Wellington: This is a more traditional equity long/short strategy, which seeks to find growth without being solely focused on pure tech companies with very high multiples. This strategy invests in growth companies worldwide, with an emphasis on the healthcare, consumer, finance and tech sectors. For example, the team may look at companies with growth products which did well for many years but then became staple products. Some of these companies may now be launching products that will become their new drivers of growth, but the market still perceives these companies as relatively steady providers of older products. Quite often, it is possible to find companies where the future growth is not yet correctly priced in.

LH: What is the role played by Chris Kirk and Dennis Kim, Schroder GAIA Wellington Pagosa’s fund managers?

Wellington: Dennis and Chris play a key role, both in picking from the 75 different strategies that we run at Wellington and in weaving them together.

This requires in-depth knowledge of all the portfolios and underlying investment philosophies. Chris Kirk joined Wellington in 2004 and is a partner overseeing the alternatives business. He has a deep knowledge of all strategies and spends a lot of time analysing and thinking about the strategic allocation.

Dennis Kim joined Wellington in 2011 and is also portfolio manager, based in Boston. He is responsible for the day-to-day risk analysis and risk management of the fund, analysing how the different strategies interact, looking at correlations and conditional correlations.

LH: Looking at all these strategies at the Fund level, how do you decide on the allocation of capital between them? Which strategies do you think are well positioned in the current and possible future market environments?

Wellington: The allocation to strategies is very strategic; the team doesn’t shift capital tactically. Different market regimes will offer opportunities in different areas, so we shift the portfolio gradually when we see that the general market regime is changing. Wellington has been managing global multi-strategy approaches for its institutional clients since 2012. In that time, we have made 10 allocation changes.

For the last eight years, we have broadly seen a post-crisis regime of low volatility and high returns across many asset classes. We think that this regime could go on for one or two more years, but we are certainly closer to the end than the beginning. That doesn’t mean there will necessarily be a symmetric shift to high volatility and low returns. Rather, we expect greater compartmentalisation of volatility and returns. It is quite possible that equity volatility will stay low even as we see a pickup of volatility in the rates and even the credit space. Such compartmentalisation has occurred in previous periods in history. With that in mind, we are gradually tilting the portfolio more towards relative-value and market-neutral strategies, which will benefit from this regime change.

LH: Would you put on any overlay trades if you noticed that two different managers or sub-strategies were making an investment on the same underlying idea?

Wellington: Yes, that can happen. We pick strategies where we feel that the portfolio managers are their own CIOs ― we don’t want to be the back-seat driver of anything that happens in the underlying portfolios. We want managers to be able to make good decisions.

Of course, we scrutinise all portfolios every day, looking at any risks that may become too big at the Fund level. We currently have one overlay, which has been on for about a year, related to the finance long/short equity team’s constructive view on interest rates. Their portfolio has exposure to banks with sticky deposits, which should benefit their interest margin most when rates go up. At the same time, our macro team also has a constructive view on rates and therefore has long positions on the short and long end of the yield curve while being short the middle part. Although these are very different ways of implementing a trade, there is a certain commonality in thinking and risk exposure. So we currently have an overlay in place, a put spread on a banking index.

LH: Multi-asset alternatives strategies are often available in hedge fund structures. How does the UCITS format of Schroder GAIA Wellington Pagosa compare? Are there any differences?

Wellington: Our partnership with Schroders is really key here. Schroders has very strong expertise in bringing alternative strategies into a UCITS format.

There are a few differences, of course. When we considered the availability of our underlying strategies, we had to leave out any which were either using too much gross exposure or addressing less liquid parts of the market. We also had to leave out strategies that trade commodities, which is not permissible in UCITS funds. Finally, we have excluded companies with a market cap below USD 500 million from the healthcare long/short strategy, in order to match the weekly dealing liquidity that we provide in Schroder GAIA Wellington Pagosa.

FOR PROFESSIONAL AND INSTITUTIONAL INVESTORS ONLY. THIS MATERIAL IS NOT SUITABLE FOR A RETAIL AUDIENCE.

All allocations described herein are for the Schroder GAIA Wellington Pagosa Fund as at 30 June 2018.

All assets under management figures are for Wellington Management as at 30 June 2018.

LH: Many thanks for the interview !

Risk considerations

Mortgage or asset-backed securities may not receive in full the amounts owed to them by underlying borrowers. The fund may be significantly invested in contingent convertible bonds. If the financial strength of a bond’s issuer (typically a bank or an insurance firm) falls in a prescribed way the bond may suffer substantial or total losses of capital. The counterparty to a derivative or other contractual agreement or synthetic financial product could become unable to honour its commitments to the fund, potentially creating a partial or total loss for the fund. A failure of a deposit institution or an issuer of a money market instrument could create losses. A decline in the financial health of an issuer could cause the value of its bonds to fall or become worthless. The fund can be exposed to different currencies. Changes in foreign exchange rates could create losses. A derivative may not perform as expected, and may create losses greater than the cost of the derivative. Emerging markets, and especially frontier markets, generally carry greater political, legal, counterparty and operational risk. Equity prices fluctuate daily, based on many factors including general, economic, industry or company news. The fund will take significant positions on companies involved in mergers, acquisitions, reorganizations and other corporate events, which may not turn out as expected and thus may cause significant losses. High yield bonds (normally lower rated or unrated) generally carry greater market, credit and liquidity risk. A rise in interest rates generally causes bond prices to fall. The fund uses derivatives for leverage, which makes it more sensitive to certain market or interest rate movements and may cause above-average volatility and risk of loss. In difficult market conditions, the fund may not be able to sell a security for full value or at all. This could affect performance and could cause the fund to defer or suspend redemptions of its shares. The fund allocates capital to multiple strategies managed by separate portfolio managers who will not coordinate investment decisions, which may result in either concentrated or offsetting risk exposures. Failures at service providers could lead to disruptions of fund operations or losses. The fund may take positions that seek to profit if the price of a security falls. A large rise in the price of the security may cause large losses.