12 Jun 2018 Alternative UCITS Market Overview May 2018

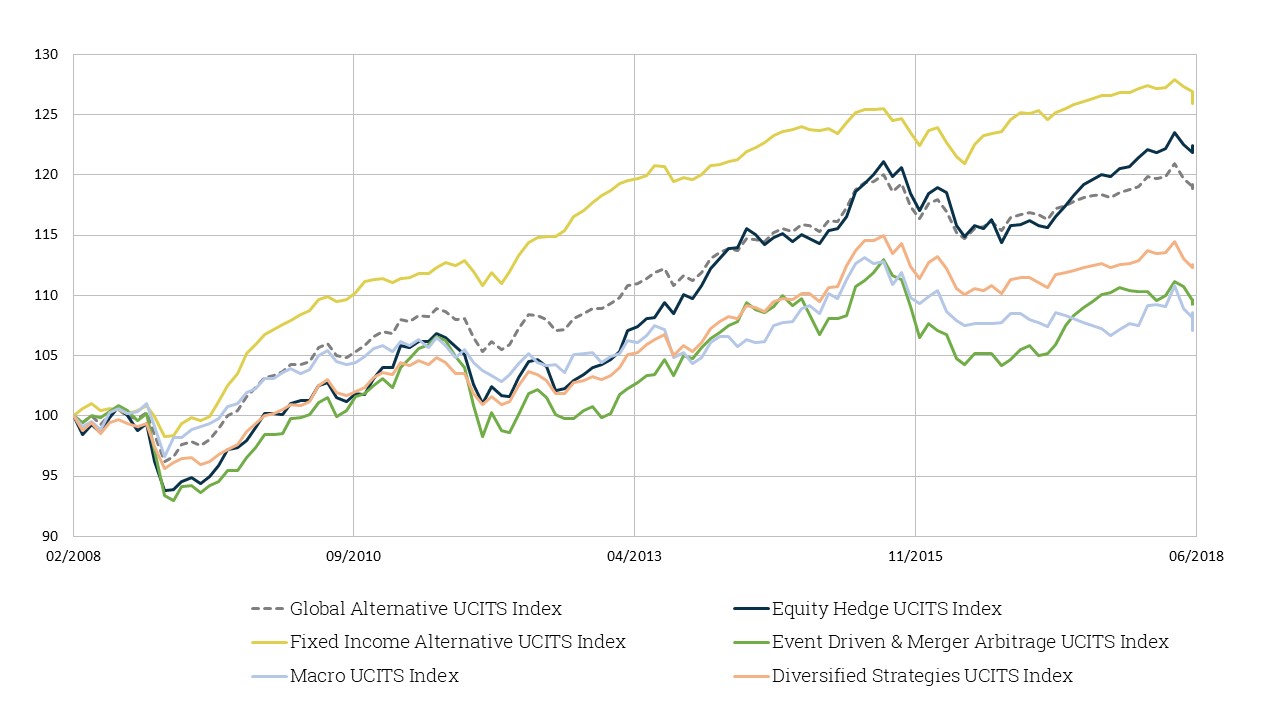

A bit more than 60% of Alternative UCITS funds posted losses in May, the LuxHedge Global Alternative UCITS Index lost -0.37%, bringing 2018 YTD to -0.83%.

Dispersion amongst Alternative UCITS funds was even more pronounced than usual with the worst fund returning -19% (leveraged Global Macro) and the top performer gaining +10% (a Long/Short AP fund).

Equity Hedge strategies held up well with most funds posting solid gains in May. Both Equity Long/Short (Index +0.17%) and Equity Market Neutral funds (Index +0.10%) avoided much of the market turmoil towards the end of the month. The largest average gains were for the Equity Long/Short US UCITS Index (+1.06%) and the Equity Long/Short AP UCITS Index (+1.65%). After a more difficult start to 2018, Event Driven and Merger Arbitrage strategies recovered ground in May: LuxHedge Event Driven & Merger Arbitrage Index +0.30%.

Against the backdrop of increased volatility due to the political situation in Italy, Discretionary Macro funds posted large losses: LuxHedge Discretionary Macro UCITS index -2.48% (YTD -1.43%). Also other multi asset strategies could not avoid negative territory with the Multi Asset Alternative UCITS Index and Diversified Strategies UCITS index declining respectively -0.24% and -0.26%.

In these more volatile market environments, investors keep allocating more to Alternative UCITS strategies with Assets under Management reaching a new record high of 470BEUR. (+1% versus last month). In line with the trend of previous months, investors mainly favoured Equity Market Neutral (AUM +4%) and Alternative Risk Premia strategies (AUM +6%).